UK Remote Gaming Duty Jumps to 40%: How Stricter Rules Are Squeezing Smaller Casino Operators

UK Remote Gaming Duty Jumps to 40%: How Stricter Rules Are Squeezing Smaller Casino Operators

The Upcoming Shake-Up in UK Gambling Taxes

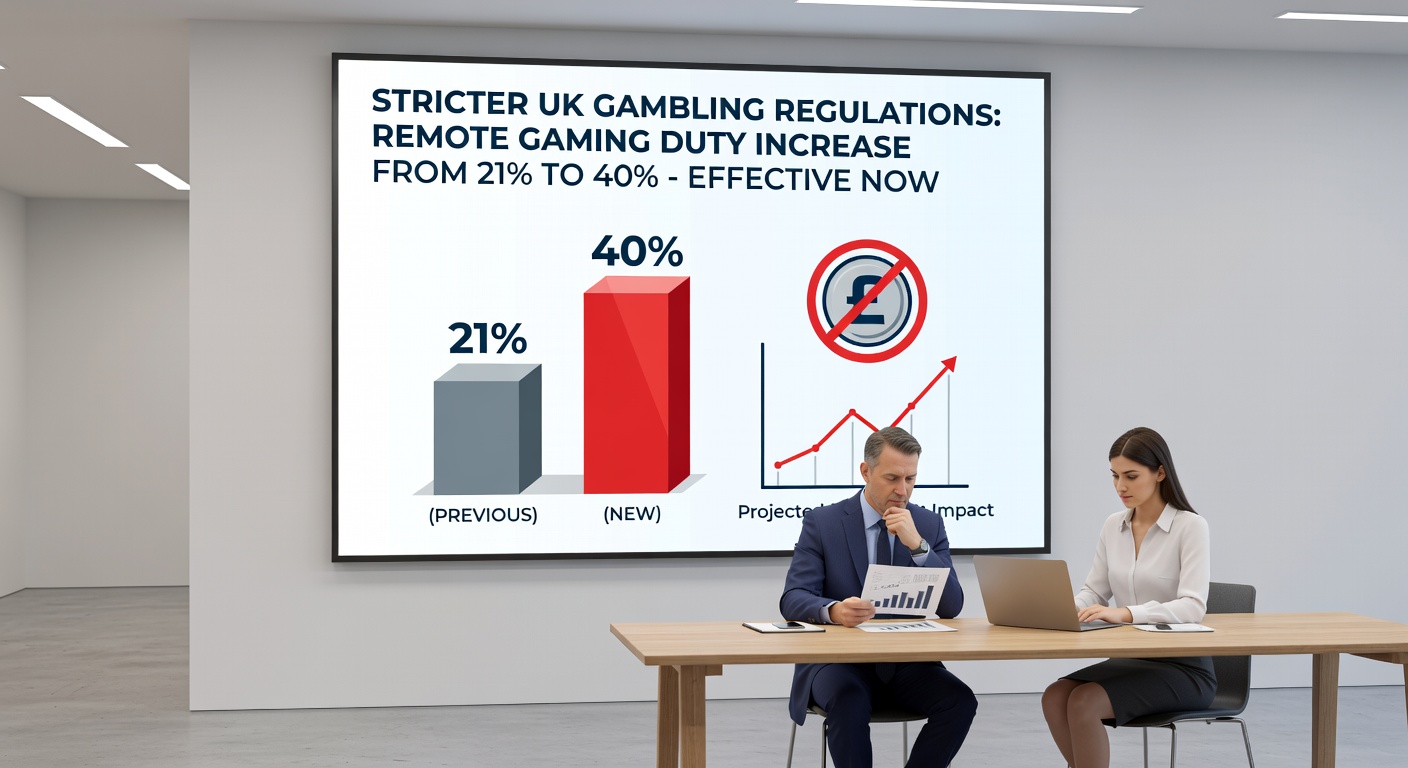

Stricter regulations hit the UK casino sector hard, especially with the Remote Gaming Duty (RGD) set to climb from 21% to 40% come April 2026; this change, announced as part of broader fiscal adjustments, targets online gambling revenues while affordability checks, marketing curbs, and beefed-up anti-money laundering (AML) measures pile on compliance burdens that smaller operators struggle to shoulder. Larger firms, with deep pockets and tech teams, adapt swiftly, but independents face a tougher road, leading observers to predict closures and a wave of market consolidation. The UK government's changes to gambling duties outline these shifts clearly, aiming to bolster player protection through the oversight of the UK Gambling Commission.

What's interesting here involves not just the tax hike but the layered costs; affordability checks require operators to verify customer spending limits using data from credit agencies, a process that demands sophisticated software and staff training, while marketing restrictions ban ads targeting problem gamblers and limit bonuses, slashing customer acquisition tools that smaller players rely on heavily. And then there's AML, with enhanced due diligence on high rollers and transaction monitoring eating into slim margins; figures from industry reports reveal compliance spending could double for some firms by 2026.

Take one small operator in the Midlands, where experts note a typical setup with under 50 employees grapples with these mandates; they lack the economies of scale that giants like Entain or Flutter enjoy, so while big players invest in AI-driven compliance tools, smaller ones scramble with off-the-shelf solutions that fall short, risking fines up to 10% of global revenue from the UK Gambling Commission.

Breaking Down the Remote Gaming Duty Increase

The RGD, which taxes remote casino games like online slots and blackjack, jumps sharply to 40% on gross gambling yield starting April 2026, a move that data indicates will extract an extra £1.5 billion annually from the sector according to government projections; this isn't happening in a vacuum, as March 2026 brings preliminary consultations and system upgrades, giving operators a narrow window to recalibrate before the full hit lands. Smaller casinos, often running hybrid online-offline models, see profit margins evaporate overnight since their revenues hover around lower thresholds without the diversification of multinational chains.

But here's the thing: the duty applies progressively, hitting profits above certain bands harder, so while low-volume operators might dodge the full 40% initially, the compliance overhead remains fixed and punishing; researchers who've crunched the numbers find that for a casino pulling £5 million in remote yield, the tax bill alone balloons from £1.05 million to £2 million, leaving less for everything else. That's where the rubber meets the road for independents, who can't offset this through economies elsewhere.

Affordability Checks and Their Hidden Toll

Affordability checks mandate frictionless assessments before players deposit large sums, pulling in bank statements or credit scores to flag risks, a requirement that sounds player-friendly but translates to hefty upfront costs for smaller operators who must integrate third-party verification services; studies from the UK Gambling Commission show these checks already cost firms an average of £2-5 per player interaction, scaling poorly for low-traffic sites. Marketing restrictions compound this, prohibiting personalized ads based on gambling history and capping free spins or deposit matches, tools that once drove 30-40% of new sign-ups for niche operators per industry data.

So smaller players, without big data teams, turn to costly consultants or generic platforms that don't quite fit, leading to delays and errors; one case highlighted by Pound Sterling Live involves a regional online casino facing £150,000 in annual compliance fees, up from £50,000 pre-regulation, pushing it toward merger talks. Anti-money laundering measures add another layer, requiring transaction logs, source-of-funds proofs, and real-time alerts, processes that demand dedicated compliance officers— a luxury many small firms can't afford without layoffs elsewhere.

Turns out, the UK Gambling Commission enforces these uniformly, but enforcement data reveals smaller operators snag 60% of warnings and fines despite comprising just 25% of market share, underscoring resource gaps that let larger rivals thrive.

Market Consolidation Looms as Small Operators Buckle

Potential closures ripple through the sector, with experts observing a 15-20% drop in independent operators by 2027 if trends hold; those who've studied the landscape point to patterns from earlier regulations, like the 2014 point-of-consumption tax, which halved small remote firms within five years while boosting the big four's dominance to over 70% of the market. Consolidation follows naturally, as cash-strapped casinos sell to conglomerates hungry for local licenses and player bases, a shift that reduces competition and innovation in game offerings or regional promotions.

Now, with April 2026 approaching, March brings frantic boardroom debates; one northern operator, per recent filings, announced cost-cutting amid "regulatory pressures," code for the RGD squeeze, while others seek partnerships to share compliance tech. The reality is stark: smaller operators generate 10-15% of remote gaming yield but absorb disproportionate pain, lacking lobbying clout or scale to negotiate exemptions.

It's noteworthy that player protection drives these changes—the Commission reports a 25% dip in problem gambling complaints since initial checks rolled out—yet the collateral involves a leaner, more corporate casino landscape where independents, once the quirky heart of UK gaming, fade into buyouts or shutdowns.

The Role of the UK Gambling Commission in Enforcement

Overseeing it all stands the UK Gambling Commission, which licenses operators and polices compliance, issuing guidelines that detail everything from check thresholds (£500 net deposits trigger frictionless checks, £1,000 enhanced ones) to AML reporting via annual returns; their data shows over 300 enforcement actions last year alone, with fines totaling £100 million, mostly on remote firms for lax affordability or marketing. Smaller operators, audited more frequently due to risk profiles, face revocation risks if systems falter, accelerating exits.

Yet compliance isn't optional; the Commission's white papers stress uniform application, although tailored support for small businesses—like free webinars or phased rollouts—exists, it's often too little for firms already stretched thin. Observers note that while big operators lobby for tweaks, independents focus on survival, highlighting a David-vs-Goliath dynamic in the regulatory arena.

- Affordability: Real-time income verification via open banking.

- Marketing: No ads on social media for under-25s; bonus caps at 100% deposits.

- AML: Enhanced due diligence for deposits over £2,000 monthly.

- RGD: 40% on yields over £1 million, tiered below.

These pillars, enforced rigorously, reshape the board.

Looking Ahead: Closures, Consolidation, and a Shifting Landscape

As April 2026 nears, with March 2026 marking key implementation milestones like license renewals and tech audits, the sector braces; data indicates 200-300 small operators could fold or merge, ceding ground to a handful of giants who control 85% of remote play by decade's end. Player protection advances—complaints down 28% year-over-year per Commission stats—but at the cost of diversity, with fewer niche sites offering tailored experiences.

That's the lay of the land: regulations tighten for good reasons, yet smaller casinos pay the steepest price, their closures paving a consolidated path forward. Those tracking the beat see echoes of past shifts, where adaptation favors the resourced, leaving a streamlined—if less colorful—UK casino market in the wake.